The Certified Financial Planner (CFP) exam is a rigorous test designed to measure a candidate’s core competency in the knowledge, processes, and ethics required of a professional financial planner.

Click “Start Test” above to take a free CFP practice exam!

CFP Eligibility

To be eligible for the CFP exam, you must meet one of the following requirements:

- You must complete a CFP Board Registered Program

- You must complete equivalent coursework subject to the CFP Board Transcript Review process

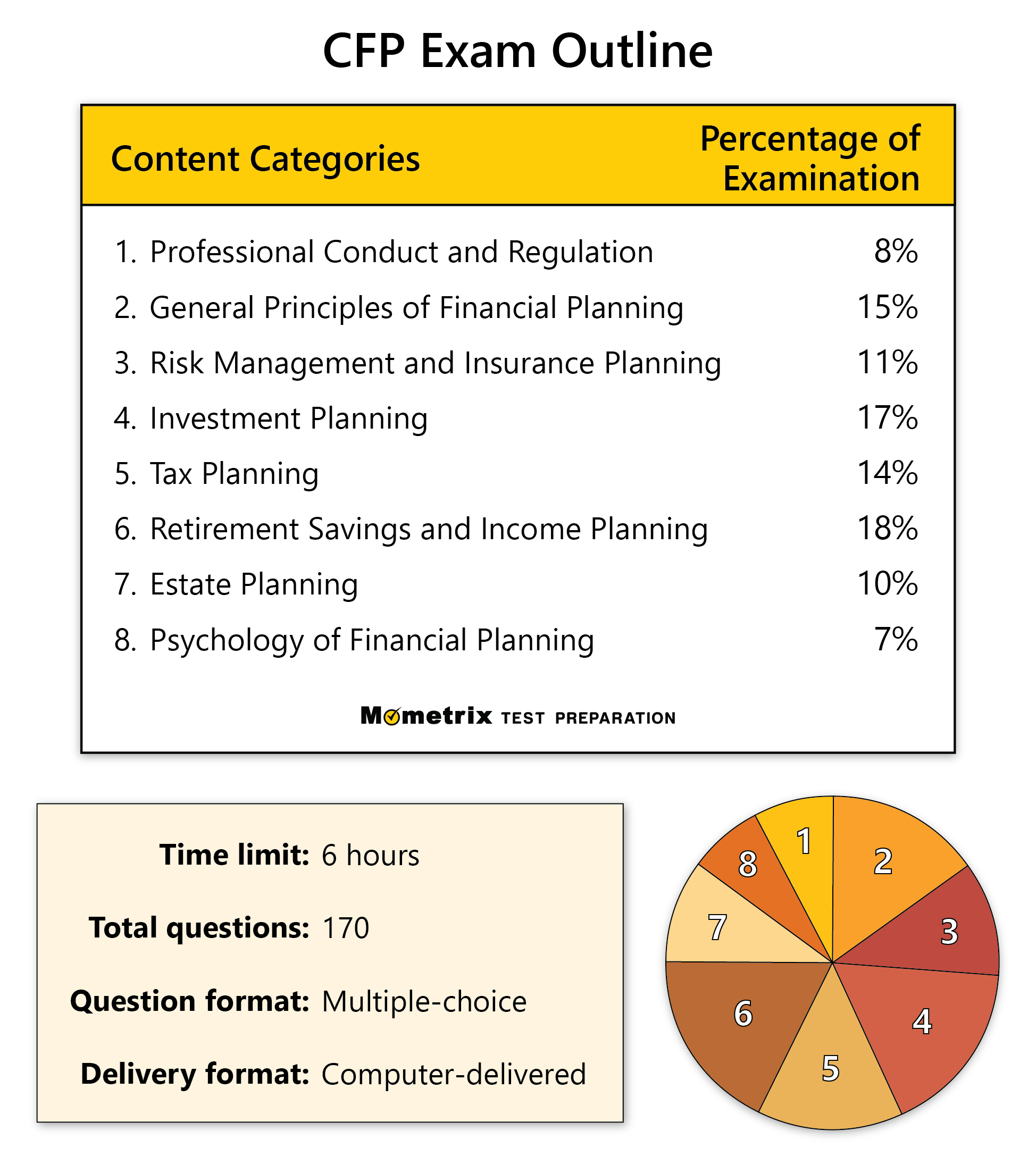

CFP Exam Outline

The CFP exam contains 170 multiple-choice questions and has a time limit of 6 hours (split into two 3-hour sections).

The exam is split into eight content domains, and each question will either be a standalone question or a scenario-based question.

1. Professional Conduct and Regulation (8%)

The questions in this domain cover the following topics:

- The function, general structure, and purpose of financial institutions

- Fiduciary standard and application

- CFP Board’s Procedural Rules

- Consumer protection laws

- CFP Board’s Code of Ethics and standards of Conduct

- Financial services requirements and regulations

2. General Principles of Financial Planning (15%)

The questions in this domain cover the following topics:

- Economic concepts

- Cash flow management

- Income tax strategies

- Financial planning process

- Time value of money concepts and calculations

- Education funding

- Financial statements

- Education needs analysis

- Financing strategies

- Debt management

3. Risk Management and Insurance Planning (11%)

The questions in this domain cover the following topics:

- Disability income insurance

- Analysis and evaluation of risk exposures

- Insurance needs analysis

- Long-term care insurance

- Principles of risk and insurance

- Qualified and non-qualified annuities

- Insurance policy and company selection

- Heatlh care cost management

- Long-term case planning

- Business owner insurance solutions

- Life insurance

- Insurance needs analysis

4. Investment Planning (17%)

The questions in this domain cover the following topics:

- Market cycles

- Alternative investments and liquidity risk

- Asset allocation and portfolio diversification

- Types of investment risk

- Investment strategies

- Characteristics, taxation, and uses of investment vehicles

- Quantitative investment concepts and measures of investment returns

- Bond and stock valuation concepts

5. Tax Planning (14%)

The questions in this domain cover the following topics:

- Current and fundamental tax law

- Income taxation of estates and trusts

- Charitable contributions and deductions

- Tax reduction techniques

- Tax implications of special circumstances

- Characteristics and income taxation of business entities

- Tax consequences of property transactions

- Tax management techniques

- Income tax fundamentals and calculations

6. Retirement Savings and Income Planning (18%)

The questions in this domain cover the following topics:

- Business succession planning

- Eldercare and special needs planning

- Key factors affecting plan selection for businesses

- Distribution rules and taxation

- Social Security and Medicare planning

- Qualified and non-qualified plan rules and options

- Retirement needs analysis

- Retirement income and distribution strategies

- Types of retirement plans

7. Estate Planning (10%)

The questions in this domain cover the following topics:

- Marital deduction

- Strategies to transfer property

- Sources for estate liquidity

- Property titling and beneficiary designations

- Planning for special needs and circumstances

- Intra-family and other business transfer techniques

- Estate and incapacity planning documents

- Planning for divorce, unmarried couples, and other special circumstances

- Postmortem estate planning techniques

- Estate, gift, and GST tax compliance and calculation

8. Psychology of Financial Planning (7%)

The questions in this domain cover the following topics:

- Principles of counseling

- Crisis events with severe consequences

- Client and planner biases, attitudes, and values

- Sources of money conflict

- General principles of effective communication

- Principles of counseling

- Behavioral finance

Check out Mometrix's CFP Study Guide

Get practice questions, video tutorials, and detailed study lessons

Get Your Study Guide

CFP Exam Registration

To register for the CFP exam, you must complete the CFP Board’s registration form and pay the examination fee. The fee for the exam increases the longer you wait to register. If you register within the first six weeks of the registration window, the fee is $825. If you register between two and seven weeks before the registration window closes, the fee will be $925. If you register in the last two weeks of the window, the fee is $1,025.

CFP Exam Dates

There are three available testing windows, each lasting eight days. Those windows are in March, July, and November and they each have a three-month registration window which closes two weeks before the actual exam week.

Once your registration is confirmed, you will be given instructions on how to schedule your exam appointment with Prometric.

Test Day

You should arrive at your testing location 15-30 minutes before the scheduled start time. When you arrive, you will be greeted by an administrator, who will ask you to sign in and present two forms of valid identification, one of which must contain your photo.

At this point, your photograph will be taken, a metal detector scan will be performed, and a digital image of your fingerprint will be captured.

You will then be asked to put any personal items in a locker, such as your cell phone, wallet, keys, and bags. Before placing any electrical devices in your locker, be sure they are completely turned off.

After your personal items have been stored successfully, you will be led to your testing station and given a brief set of testing instructions before the exam begins. The exam is split into two 3-hour sections with one scheduled 40-minute break between sections.

How the CFP Exam is Scored

This is a pass/fail exam, which means that the exact score you get does not matter, as long as it is at or above the cutoff. You’ll find out your results at the testing center immediately after completing the exam, but you’ll have to wait about four weeks for your official score report to be sent to you by mail.

If you did not pass, you will receive a diagnostic report to help you see where your weaknesses are and how to improve for your next attempt. If you did pass, you will simply receive instructions for the next steps in the certification process.

Retaking the CFP Exam

If you fail the exam, you may retake it up to five times in your lifetime.

Check out Mometrix's CFP Flashcards

Get complex subjects broken down into easily understandable concepts

Get Your Flashcards

FAQs

Q

What is the CFP exam pass rate?

A

The current pass rate of the CFP exam is 64%.

Q

How many questions are on the CFP exam?

A

There are 170 multiple-choice questions on the exam.

Q

How long is the CFP exam?

A

The time limit for the CFP exam is 6 hours, not including a scheduled 40-minute break between sections.

Q

What is the passing score for the CFP exam?

A

The exact score you need in order to pass the CFP exam is unknown, though many speculate that you must answer at least 70% of the questions correctly to pass.

Q

How much does the CFP exam cost?

A

The examination fee for normal registration is $925.